Story summary

Wakefield’s theory

The New Zealand Company played an important role in the European settlement of New Zealand. A major figure in the company was Edward Gibbon Wakefield. He made the adoption of new colonies part of economic debates in the United Kingdom.

Wakefield felt that colonies added land and new opportunities for work, and lessened conflicts between landowners, land developers and workers. He argued that land should be sold for a ‘sufficient price’, so labourers had to save to buy it over time.

Single tax

The single tax movement had a big influence on 19th century economics. People felt that only land should be taxed. They wanted a tax which targeted the ‘unearned increment’ – the increased value of land even if it had not been developed.

Free trade

In the 1860s the government was anxious to adopt free trade, with no taxes on imports. But it relied on duties like tariffs (which were charged for imported goods) for its income. Tariffs were renamed ‘revenue tariffs’ and were targeted at imported luxuries. British economist John Stuart Mill suggested tariffs could be used to protect ‘infant industries’, new businesses which needed time to grow and compete in the market. The New Zealand government used local infant industries to justify some taxes on imports.

Measuring growth

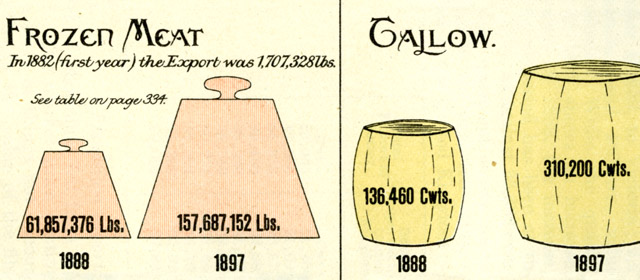

In the 19th century governments could only measure the growth of the economy in indirect ways, such as counting exports or imports. This often led to unreliable statistics. New Zealander Charles Knight realised that outputs from one industry could feed into another industry, so the combined growth of all industries differed from the total industrial output available to consumers.

Economists

Economics was not a profession until the 20th century and was taught as part of other subjects like philosophy at universities.

James Hight taught a generation of budding economists at Canterbury College (now university) some of whom had distinguished careers overseas. Students’ exams were sent to the UK for marking and world-famous economist John Maynard Keynes marked some of them. Students did very well.

1930s depression

Keynes’s ideas about government spending influenced New Zealand economists like Horace Belshaw and Douglas Copland who advised the government during the 1930s economic depression.

The depression changed economic thinking. Economists were taken more seriously, and governments were more willing to intervene in economies following their advice.

Statistics

As the discipline of economics developed, governments had more sophisticated ways to measure economic change, using econometrics.

Economists overseas

New Zealand has mostly followed, rather than led, economic thinking. But the country has produced some distinguished economists, including Rex Bergstrom in the field of econometrics and Ronald Meek on laissez-faire French economics. The best-known New Zealand-born economist was Bill Phillips. He invented the MONIAC machine to demonstrate the relationship between unemployment and inflation.

Market forces

Economists debate whether governments or markets should carry risks in the economy. After the 1980s New Zealand relied more on market forces to manage risk. Markets are not always appropriate for managing environmental impacts. However economists have devised ways to measure and manage these ‘externalities’, costs or benefits with no market value.